Causes of the rapid rise in services prices

(Authors: Kamila Kulhavá, Luboš Růžička, Radek Šnobl)

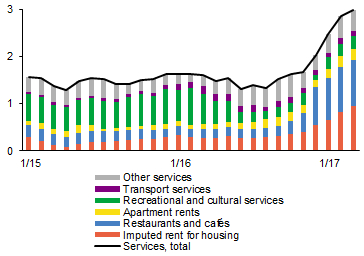

Non-tradable goods price inflation surged at the turn of the year, especially in two components. Specifically, these were prices in restaurants and cafés and imputed rent for owner-occupied housing (see Chart 1). This box takes a closer look at the causes and persistence of these developments.

Chart 1 (BOX) Non-tradable goods inflation

The contributions of restaurant services and imputed rent have increased significantly in recent months

(contributions to year-on-year growth in percentage points)

The increase in prices in restaurants and cafés was due among other things to the launch of electronic sales registration (ESR). Prices in this segment increased sharply despite a cut in the VAT rate applying to restaurants and other catering facilities from 21% to 15% with effect from December 2016. In addition to ESR-related costs, food services firms seem to have reflected in higher prices the effect of the increase in the minimum wage and wage growth in the economy in general, which for them implies long-term growth in personnel costs. ESR concentrated the pass-through of these fundamental cost effects to prices into a short time span. Renewed growth in food prices also accounted for part of the upswing in prices in this category. By its very nature, the effect of the launch of ESR on price growth will be only temporary, as already evidenced by month-on-month growth of prices in restaurants and cafés. During 2017 Q1, it fell gradually to levels common before ESR was introduced. Conversely, wage growth will continue to push up prices in food services and services in general.

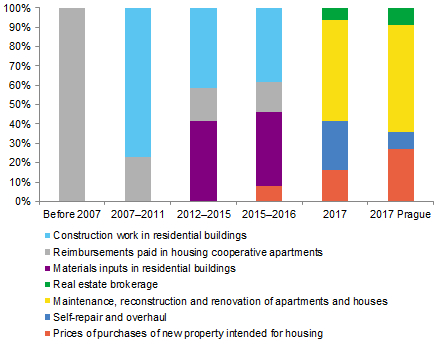

The rise in the growth rate of imputed rent was linked with an increase in the weight of new property prices, which are currently rising rapidly. At the end of 2016, the CZSO changed the structure of imputed rent. The weight of new apartments jumped from 8% to 16.3% for regions outside Prague and to 27% in Prague (see Chart 2). These and previous changes together imply a gradual replacement of imputed rent by owner-occupied housing in the form of the net acquisition approach. This approach captures households’ total property purchase expenditure, including spending on home improvements and maintenance and related services, net of their total property sale income. This concept thus covers new property prices in addition to the consumption component. It can therefore be viewed as a broader macrofinancial index partly linking elements of monetary policy and financial stability. This is because it opens up more space for capturing growth in prices of new apartments, which is currently very strong in Prague, directly in consumer price inflation. It can be expected that the growth in new property prices will not be temporary and that the higher inflation in this segment will persist over the forecast horizon.

Chart 2 (BOX) Weighting scheme for imputed rent

The weight of prices of new property intended for housing in imputed rent has been increased in several steps

(percentage shares of components of imputed rent index)