An experimental price index including prices of older properties

(Authors: Luboš Růžička, Radek Šnobl)

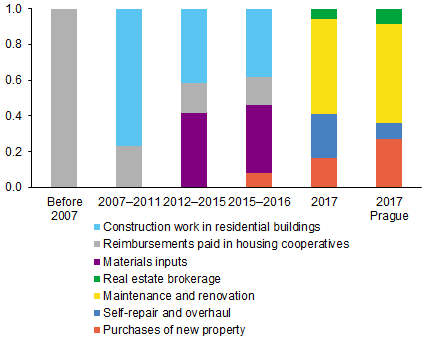

The consumer price index weighting scheme is changed on an ongoing basis. The latest change increased the weight of new property prices.1 This step by the CZSO was a follow-up to a mid-2015 adjustment representing the first weakening of the rental equivalence approach,2 with an estimate of prices of new residential property purchases incorporated into imputed rent for the first time,3 although with a only relatively small, 8% weight (see Chart 1). This weight was increased to the current 16.3% (and as much as 27% in Prague) at the start of 2017. The current structure of the consumer price index (CPI) thus better reflects growth in prices of new apartments, which is currently very strong in Prague. The steps have brought imputed rent in the consumption basket closer to the owner-occupied housing index in the form of the net acquisition approach. The latter takes into account households’ expenditure on property purchases from other sectors and related services (including spending on home improvements and maintenance) net of their total property sale income.

Chart 1 (BOX) Weighting scheme for imputed rent

The CZSO increased the weight of prices of new property intended for housing in the calculation of imputed rent

(percentage shares of components of imputed rent index)

However, the net acquisition approach within the CPI does not cover the predominant transactions in older property between households.Prices of property, including older property, can nevertheless be tracked using the house price index (HPI).

The HPI can be used to calculate an experimental CPIH price index, which can be viewed as a wider macrofinancial indicator. It departs from the traditional CPI concept, as it does not strictly separate household expenditure depending on whether consumption or investment components prevail in it. It is therefore not a standard measure of households’ living costs, which monetary policy traditionally focuses on, but an indicator that can potentially be used to integrate monetary policy and financial stability considerations. A look into the past reveals that the year-on-year change in the CPIH index was 0.7 percentage point below CPI inflation due to a decline in property prices in 2010–2012. The two indicators subsequently converged in 2013 (see Chart 2). Property price growth, which has been accelerating since 2014, is opening up the gap in the opposite direction. In 2017 Q1, inflation as expressed by the experimental index was almost 3.9%, i.e. 1.4 percentage points above consumer inflation.4

Chart 2 (BOX) The experimental CPIH price index

The experimental CPIH price index was below consumer price inflation until 2013, but has been rising faster since 2014 and is currently showing growth of almost 4%

(annual percentage changes; source: CZSO and CNB)

The index constructed in this way should be viewed as an analytical tool; 2% inflation as captured by the CPI remains the CNB’s target.Nevertheless, one can discuss the signals the CPIH index would send to monetary policy makers if they wanted to take prices of older property explicitly into account.5 During the recession and the related decline in property prices in 2012 and 2013, a hypothetical monetary policy focus on such an extended indicator would, other things being equal, have resulted in a need for even easier monetary policy than that under the inflation targeting regime. By contrast, the index would currently imply a need for a greater tightening of monetary policy due to a pronounced rise in property prices in the secondary market. In this context, however, one should bear in mind that the CNB’s monetary policy focuses not on current inflation but on inflation 12–18 months ahead. So, to take into account prices of older property in monetary policy, the central bank would first need a forecast for such prices that is fully linked to its overall macroeconomic forecast. It should be noted, however, that the CNB has already responded to the signals of property market overheating by tightening macroprudential policy, which is a more appropriate tool for such purposes than monetary policy instruments.

1 See Box 3 in Inflation Report II/2017.

2 Over the last ten years, this approach has to a large extent taken into account the index of construction work prices in apartment buildings, the index of material input prices in apartment buildings and the index of prices of payments made in cooperative apartments.

3 Imputed rent has a weight of around 8.7% in the CPI.

4 The HPI is available with a lag of one quarter longer compared with the CPI. This disadvantage naturally transfers to the CPIH experimental index.

5 This issue is addressed in detail in the recently published Research and Policy Note CNB RPN 1/2017 by M. Hampl and T. Havránek: Should Inflation Measures Used by Central Banks Incorporate House Prices? The Czech National Bank’s Approach.