Monetary policy transmission is working

Since the exit from the exchange rate commitment in April 2017, interest rates have again been the Czech National Bank’s main monetary policy instrument. The CNB has increased rates seven times since then. After the exit, the koruna started appreciating as expected, so the exchange rate helped tighten the monetary conditions. In February 2018, however, the exchange rate trend changed.

This blog article focuses on a question that has naturally appeared in the media in this context: Does the recent koruna exchange rate trend reflect ineffective monetary policy, and is – to use economic jargon – its transmission therefore impaired? Our answer is no. In the article below, we will discuss the factors behind exchange rate movements, including the size of the international reserves and the koruna positions of foreign investors, and the functioning of monetary policy transmission in general.

The koruna stopped appreciating in spring 2018

Let’s begin by explaining the context of recent developments. Until 2017, the CNB used the exchange rate as an additional instrument of monetary policy. A large amount of euros was purchased in foreign exchange interventions, especially as the exit from the commitment neared. In total, almost EUR 76 billion was bought while the commitment was in place. Since the exit, the CNB has not intervened in the forex market. The koruna firmed slightly after the commitment was ended in 2017, reaching CZK 25.20 to the euro in early 2018 (see Chart 1). This appreciation had been foreseen by the CNB in its forecasts prepared – but at the time still temporarily unpublished – last year. Like financial market analysts, the forecasts had predicted a strengthening koruna for several reasons. The first was a widening interest rate differential. The CNB began raising its rates in summer 2017, whereas the European Central Bank is still keeping its rates negative and is continuing its quantitative easing. An equally important reason was renewed real equilibrium appreciation of the koruna, connected with economic catching-up with advanced countries and growth in domestic productivity.

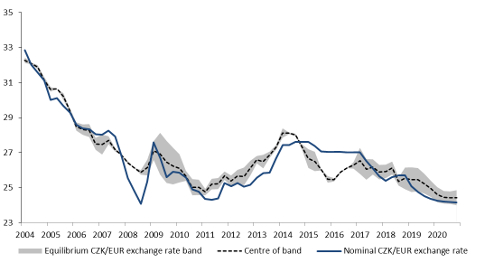

Chart 1: The exchange rate of the koruna against the euro

(CZK/EUR)

Source: CNB

In March 2018, the appreciation halted, and in the following months the koruna has been flat, or rather has weakened slightly to a current level of just below CZK 26 to the euro. This reversal in trend was due mainly to worsening global sentiment and related asset sales in emerging markets. For historical reasons, some investors continue to rank the Czech Republic among these markets. The deterioration in sentiment was due to many factors, most notably crises in Argentina and Turkey, growing protectionist tendencies in global trade, an increasing threat of a hard Brexit, growth in US rates and concerns of a hard landing of the Chinese economy. Alongside these, what we might call psychological, factors, one material factor fostered slower appreciation in 2018: a slightly lower net inflow of foreign currency onto the current account (due to muted growth in the domestic car industry, the until recently high oil prices and developments in wage transfers and private transfers). Towards the end of the year, it was joined by the now almost traditional, relatively technical – or rather seasonal and hence temporary – factor of commercial banks trying to downsize the deposits on their balance sheets at the year-end because of the requirement to contribute to the resolution fund. For this reason, banks try to deter large institutional depositors, often foreign ones, by applying penalty fees or negative interest rates on large deposits held over the year-end. This motivates many foreign investors to close their koruna positions (often only temporarily) and puts the koruna under short-term depreciation pressure. A year ago, this effect quickly dissipated right at the start of January and the koruna appreciated.

According to the CNB’s latest estimates, the koruna is currently slightly undervalued.1 However, the degree of undervaluation is modest and not excessive in historical terms. The current CNB forecast expects the real exchange rate of the koruna to strengthen over the next year, initially close to its equilibrium level and later only slightly below it (see Chart 2).

Chart 2: Estimate of the nominal equilibrium exchange rate

(CZK/EUR)

Source: CNB

What is the effect of overboughtness?

Another hypothesis explaining the koruna’s current level is “overboughtness” of the koruna market. The CNB’s communications around the time of the exit from the commitment stated it transparently as a factor that might dampen the koruna’s appreciation driven by the above fundamentals. It is true that the koruna assets of non-residents have been substantially higher in recent years than in the more distant past. The overboughtness hypothesis assumes that, for some time to come, the supply of foreign exchange arising from the foreign currency income of Czech entities will not be enough to cover the foreign exchange demand that would arise if non-residents wanted to close their positions all at once. This essentially means that the koruna should appreciate at a pace inconsistent with real convergence and the positive and widening interest rate differential for a while yet. Given the appreciation of the koruna observed over the first ten months following the exit from the commitment, however, we believe that the contribution of koruna market overboughtness to the currently weakened exchange rate is less significant than that of global sentiment.

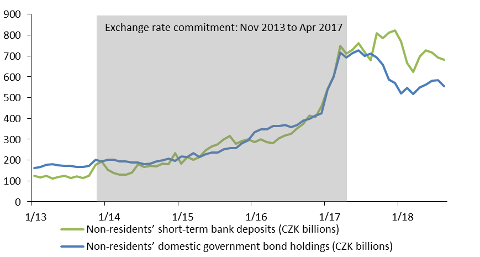

Our view is supported by the evolution of non-residents’ koruna assets. Almost two years have passed since the exchange rate commitment ended. The initially hot money speculating on a rapid strengthening of the koruna shortly after the exit is therefore gradually but inevitably cooling. Foreign investors reduced their domestic bond holdings in 2017, whereas in 2018 non-residents’ domestic bond holdings were flat (see Chart 3). Non-residents’ koruna deposits at Czech banks swung up and down in the period under review, rising slightly in 2017, but falling markedly in early 2018, only to go up modestly again in the summer. In August, the total volume of these assets was about CZK 200 billion lower than at the time of the exit. We can infer from this that efforts by foreign investors to close their Czech koruna positions could have had a particularly significant impact on the koruna exchange rate in the second half of 2017 and in early 2018. At that time, though, the koruna was appreciating.

Chart 3: Non-residents’ koruna assets

(CZK billions)

Source: CNB

The CNB sees uncertainty regarding the future exchange rate path and captures it in a sensitivity scenario

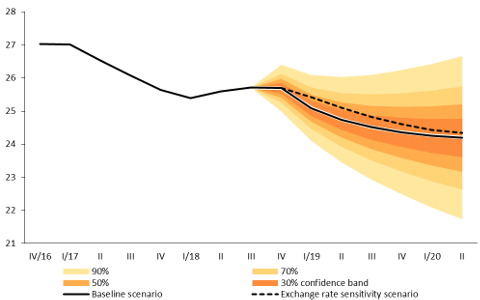

The CNB’s forecasts take account of all the available economic information, including the negative global sentiment. The current forecast, published in November 2018, expects these effects to continue to dampen the appreciation of the koruna next year but to gradually fade during the first half of 2019. In the baseline scenario of the forecast, the koruna is thus expected to appreciate below CZK 25 to the euro in spring 2019 and below CZK 24.50 to the euro in late 2019. This expected appreciation will be driven by the same fundamental factors as in the past.

The duration of the global factors associated with the change in sentiment on global markets recently affecting the koruna is a risk to this forecast. The outlooks of other entities indicate a weaker exchange rate one year ahead than the CNB forecast, amid higher interest rates and a similar inflation prediction. The risk of a weaker-than-forecasted exchange rate was described in a sensitivity scenario in the most recent Inflation Report IV/2018. The pressure for a longer-lasting depreciation in the sensitivity scenario leads to a distinctly higher interest rate path than in the baseline scenario of the latest forecast. Monetary policy thus responds with a significant increase in interest rates to prevent the stronger inflation pressures which a markedly weaker exchange rate would otherwise create via faster growth in import prices. The increase in interest rates widens the interest rate differential and counteracts the depreciation pressure, although it cannot fully prevent it (see Chart 4). In this scenario, inflation thus returns to the target somewhat later than in the baseline scenario of the forecast.

Chart 4: Exchange rate sensitivity scenario

(CZK/EUR)

Source: CNB

The central bank is thus in a relatively comfortable position in this regard: if the monetary conditions need tightening in the current cyclical situation, it can do so by raising interest rates more markedly if the depreciation pressure on the koruna persists. It always has enough ammunition to tighten monetary policy, and there is nothing to prevent interest rates from returning to their equilibrium level faster than currently expected, or even from going above it (because the sky is the limit).

By contrast, the calls for the CNB to actively reduce its reserves to deliver exchange rate appreciation cannot be regarded as justified. In the current situation, selling international reserves would be an unsystematic intervention in the functioning of the foreign exchange market and the exchange rate. Such a measure would also be counterproductive, in that it would further weaken the effect of fundamentals on this key economic variable and introduce uncertainty into the functioning of monetary policy transmission. Of course, renewing the programme of sales of part of the income on the CNB’s international reserves remains an open option for the future. This programme was suspended temporarily in 2012. However, this is not an issue the CNB is currently considering. Any renewal of such sales would in any case be conducted so as to minimise the impact of the programme on the exchange rate.

Has monetary policy transmission really been weakened?

To answer the question of whether the transmission mechanism is at risk, as is sometimes asked in relation to the CNB, let’s now take a look at another important channel of monetary policy transmission – the interest rate and credit channel. Monetary policy rates should ideally pass through relatively quickly to the interest rates banks charge or pay their clients, in particular rates on household and corporate deposits and loans. An abnormal change in the spreads between the relevant interest rates would be a signal of potential problems in the functioning of transmission.

Before the exchange rate commitment was introduced, very rapid transmission was typically observed for corporate loans. The difference between the rate on loans to corporations and the CNB repo rate averaged 1.8 percentage points over 2004–2012. So far in 2018, the difference has been 1.7 percentage points. No drastic difference is therefore visible.

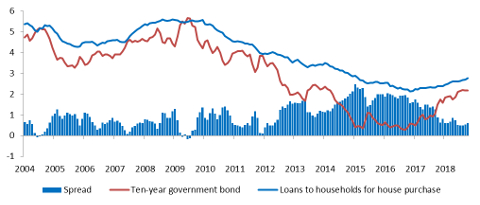

Loans to households for house purchase are another illustrative example of the functioning transmission of monetary policy rates to client rates. Sufficient market competition and a relatively homogeneous product ensure that banks usually react across the board and relatively soon to financial market developments, and rates on new loans have a clear tendency to follow market rates. This is again evidenced by a comparison of the spread between the mortgage rate and long-term financial market rates, which are relevant to the interest charged on housing loans: in 2004–2012, the average spread between the rate on housing loans and the ten-year government bond yield was 0.7 percentage point; so far in 2018, this spread has been 0.6 percentage point (see Chart 5).

Chart 5: Spread between the ten-year government bond yield and the interest rate on new loans to households for house purchase

(%, percentage points)

Source: CNB

Until recently, average client consumer credit rates were falling steadily from previous high levels. This reflected stronger competition and perhaps also a rise in the financial literacy of the Czech population, as manifested in a gradual decrease in banks’ interest margins, which had previously been well above the euro area average. The turnaround of the interest rate trend in this specific credit segment due to the upward shift of the financial market yield curve has therefore been slow to arrive. Transmission is thus very difficult to analyse using the available data. For the structural reasons mentioned above, monetary policy transmission in this credit segment was not very strong even before the exchange rate commitment was introduced.

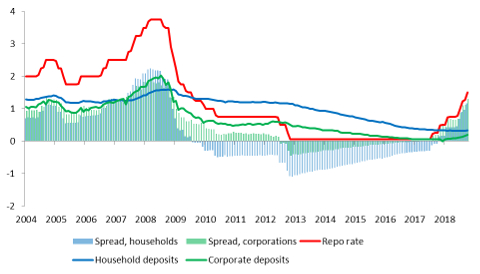

According to the latest data, deposit interest rates do not indicate any failure in transmission either. The observed data show that the spread between client and market rates attained both strongly positive and negative levels in the past (see Chart 6). The zero lower bound on interest rates, which was very relevant to the Czech banking sector, played a role here. In 2004–2012, i.e. before the exchange rate commitment was introduced, the average spread between the CNB’s two-week repo rate and the rate on koruna deposits accepted by banks from households and corporations was 0.5 and 0.8 percentage point respectively. So far in 2018, it has averaged 0.6 and 0.8 percentage point respectively. So, the pass-through of monetary policy rates to deposit rates has not worsened dramatically either.

Chart 6: Spread between the CNB repo rate and the interest rate on koruna deposits accepted by banks from households and corporations

(%, percentage points)

Source: CNB

The above evidence suggests that the transmission of changes in monetary policy rates to client rates has not been tangibly disrupted in any of the areas examined.

The next phase of the transmission of interest rates to the economy may be weakened by the rise in the share of foreign currency loans in corporate financing observed in recent years. Interest rates on these loans are derived from foreign yield curves and are therefore not affected by CNB monetary policy. The share of these loans was 18% in 2004–2012 but has increased since then, to the extent that foreign currency loans today account for 30% of all corporate loans. This reflects the high openness of the Czech economy. Foreign currency loans (and deposits) are concentrated mainly in corporations involved in international trade. Such loans are used partly as natural hedging against exchange rate risks by exporters and also, for example, by domestic developers. These entities match their future foreign currency income and foreign currency loan instalments, thereby reducing their exposure to exchange rate risk. However, the share of foreign currency loans to corporations can be expected to decrease as euro area interest rates increase.

Foreign currency loans to households are virtually non-existent, so the overall share of foreign currency loans to corporations and households in total bank assets is very low, currently standing at around 6%. So far, no other changes or problems in the interest and credit transmission channel have been observed either.

The transmission of CNB monetary policy is working

The central bank will always face uncertainty as to whether its view of current economic developments is correctly calibrated. The CNB therefore systematically monitors and analyses the latest economic and monetary developments and the ensuing potential risks to its forecasts. Recently, its attention has been focused on the exchange rate as the main uncertainty of the forecasts. However, the very orderly course of the current business cycle and the successful fulfilment of the inflation target following the exit from the exchange rate commitment show that the CNB’s monetary policy arsenal is sufficiently effective. This is true both of its instruments directly and of its capacity to maintain the essential confidence of experts and the public in its ability to anchor inflation expectations and stabilise the economy. In short, the transmission of CNB monetary policy is working.

1 The CNB estimates the equilibrium exchange rate using the BEER (behavioural equilibrium exchange rate) and the FEER (fundamental equilibrium exchange rate) methods. For details, see this blog post (in Czech only).