Graph of Risks to the Inflation Projection (GRIP)

8th Situation Report 2018

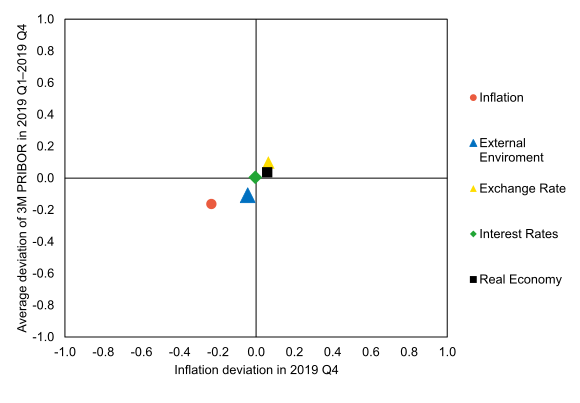

The Monetary Department assesses the balance of risks to the Inflation Report IV/2018 forecast as being broadly balanced. In the GRIP simulation, the effect of the individual risks arising from the newly published data is slightly anti-inflationary overall. The main anti-inflationary factor is lower observed domestic inflation, which was largely a result of an unexpected fade-out of growth in volatile food prices. To a smaller extent, a revised outlook for foreign variables also has an anti-inflationary impact in the simulation. Conversely, a slightly weaker exchange rate in Q4 has a slightly inflationary effect. As regards other data from the domestic economy, the forecast is materialising well in qualitative terms, the deviations from the forecast being mostly moderate and partial.

Outside the GRIP simulation, the risk of negative global market sentiment having a longer-lasting effect on the koruna’s exchange rate persists. In Inflation Report IV/2018, this risk was captured by an exchange rate sensitivity scenario in which pressures for further depreciation of the koruna led to significantly higher interest rates than in the baseline scenario of the forecast. On the other hand, the current decline in global oil prices is an anti-inflationary risk outside the GRIP. Uncertainties connected with protectionist tendencies in global trade and with the manner of exit of the United Kingdom from the European Union still persist.