Graph of Risks to the Inflation Projection (GRIP)

6th Situation Report 2018

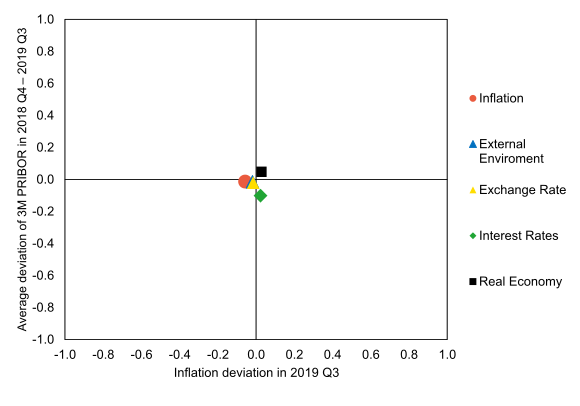

The Monetary Department assesses the balance of risks to the Inflation Report III/2018 forecast as being balanced and the individual risks as being insignificant with regard to both future inflation and interest rates. A slightly revised outlook for foreign variables and new data from the domestic economy both have an almost neutral effect in the simulation. As expected, growth in economic activity slowed amid continuing high wage growth and increasing employment. Observed inflation was slightly lower than forecasted due to a significant drop in food price inflation (in line with the sensitivity scenario in Inflation Report III/2018). However, the drop was largely offset by a more distinct acceleration of core inflation. In addition, the outlook for future administered price inflation is increasing. The exchange rate appreciated slightly more on average in Q3 than expected. The risks of a different exchange rate path, as captured in the second sensitivity scenario in the latest Inflation Report, are thus not materialising as yet.

Outside the GRIP simulation, uncertainties stemming from growth in protectionist measures in global trade and Brexit-related events persist.