Graph of Risks to the Inflation Projection (GRIP)

4th Situation Report 2018

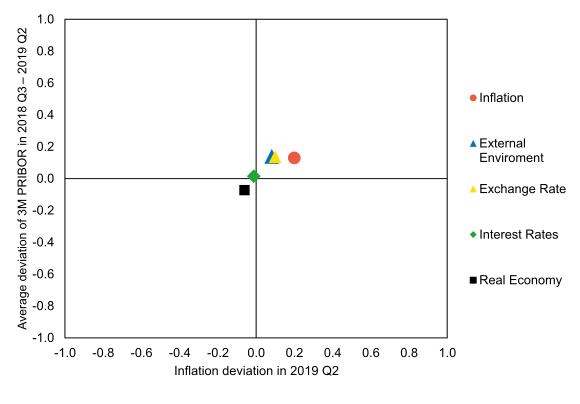

The Monetary Department assesses the balance of risks to the Inflation Report II/2018 forecast as being inflationary and tilted to a higher interest rate path. The slight effects of higher domestic inflation, a weaker exchange rate and a higher external price outlook are acting concurrently in this direction in the GRIP simulation. The effect of the domestic real economy is only slightly anti-inflationary compared to the forecast. Movements in domestic interest rates are in line with the forecast.

Outside the GRIP simulation, these inflationary risks might be further intensified if the exchange rate were to remain weaker in the quarters ahead compared to the current forecast. The forecast expects the exchange rate to appreciate sharply in the next quarter, but the global factors fostering the currently weaker-than-forecasted levels of the exchange rate are likely to persist over a prolonged period. On the other hand, the external risks surrounding economic growth have recently intensified downwards.